aNewDomain — SoftCard, the failed mobile payment joint venture from the major wireless carriers, announced this week its service will officially cease to work on March 31. This is a result of Google’s recent purchase of the company. And the official close of business ends another chapter in the never-ending story of shortsightedness by the major wireless carriers in the United States, a shortsightedness that enriches others and is a litany of lost opportunity and income.

Here’s the anatomy of yet another wireless carrier failure.

2005: When Verizon Rejected the Apple iPhone

In 2005, when the first Apple iPhone was in mid-development, AT&T Mobility was known as Cingular. Back then, Verizon was the undisputed leader in the business. Cingular at the time was the second largest carrier behind Verizon, but it still was a relatively young company — the fairly new result of a consolidation of twelve regional carriers.

In February 2005, Apple CEO Steve Jobs began the process of courting wireless carriers to carry the iPhone in such a way that it gave Apple unprecedented control over systems and services. And in the middle of extended negotiations with Cingular for exclusive rights to the iPhone, Jobs met with Verizon officials to discuss the possibility of releasing the iPhone exclusive ly on Verizon instead.

ly on Verizon instead.

Verizon infamously rejected Jobs outright, and the rest is history.

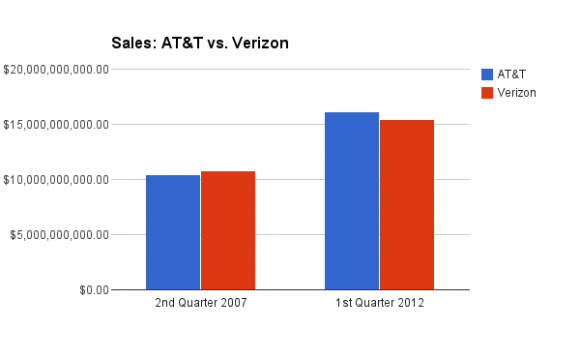

2007: AT&T Takes Apple iPhone Exclusivity to the Bank

Cingular in 2007 began the process of rebranding to AT&T, and released the iPhone with a guaranteed four years of exclusivity.

In the second quarter of 2007, at the beginning of its exclusive iPhone run, AT&T trailed Verizon in sales by $400 million. But by the first quarter of 2012, when the exclusive period ended and other carriers began to carry the iPhone, AT&T led Verizon in sales by $700 million.

2008: Carriers Miss the True Value of Text Messaging

In 2008 text messaging was at an all time historical high. So were texting prices.

Unlike most plans today, texting was an additional add-on service back then, with prices in the range of $5 a month for 200 text messages to $20 a month for unlimited texting. If you didn’t have a plan, or you went over the plan amount, you were charged on a pricey per-text basis. So not fun.

That year, two seemingly unrelated events changed the trajectory of messaging. First, app stores on Android and iOS launched in the form of Google Play and Apple iTunes.

Second, the major carriers raised text pricing from 10 cents a text to 20 cents a text.

This was a grave error.

While the high fees for texting led to short-term profits, the consumer outcry was palpable. The consumer outcry led to accusations of collusion amongst the carriers, who in 2009 testified in front of U.S. Senate Subcommittee on Antitrust, Competition Policy, and Consumer Rights, in an attempt to justify the high costs.

Meanwhile, the beginning of the app revolution was taking place on smart phones, and text messaging was ripe for disruption. Apps that offered messaging for little to no fee became early hits in the mobile app stores, with apps such as WhatsApp and Kik Messenger showing meteoric rises in users almost immediately.

By 2012, messaging apps continued to rise in popularity, while carriers, still charging for messaging plans, started to experience a decrease in texting.

Big surprise.

While experience short-term profits, the carriers, once again, missed the big picture: the true value of messaging is not the service itself, but the data the service produces. The connections between user is the real value. The value of such connections led Facebook to purchase WhatsApp, an otherwise unremarkable app with a huge user base, for $16 Billion in 2014. Today, the users -and data-have mostly migrated to apps; and the carrier profits for text messaging are mostly gone, with most plans including unlimited texting free with data plans.

2011: And Then Came the Blocking of Google Wallet

In 2011, Google announced Google Wallet, a service that allowed consumers to tap and pay with NFC-enabled Android phones. A fairly straight-forward and useful service with one glaring problem: it was available on Sprint only.

Verizon, AT&T, and T-Mobile all blocked Google Wallet, opting instead to only support SoftCard (originally labeled with the now unfortunate name ‘ISIS’).

SoftCard launched as a mobile payment joint venture between Verizon, AT&T and T-Mobile.

And as we see now, it failed spectacularly.

In its wake, it essentially grounded Google Wallet before it could ever get off the ground. In the end, Apple eventually launched Apple Pay in 2014 with no resistance, and Google purchased SoftCard, essentially having to start over in the mobile payment field, playing catchup to Apple.

What’s Next?

Given the multitude of missteps and failures, it seems clear the entire wireless industry is ready to be disrupted. Noted technology journalist Paul Thurrott suggests as much, comparing the wireless carriers to the lumbering automobile makers of the 1970’s and early 80’s. He goes on to suggest who better to do so than Google, who just announced a planned hybrid cellular/wifi service.

Maybe it will be Google that disrupts the wireless industry. Or maybe someone else. No matter who is it, you can be sure that no matter what direction the big carriers are moving, the disruptor will be headed in the opposite direction.

For aNewDomain, I’m Mike Olsen.